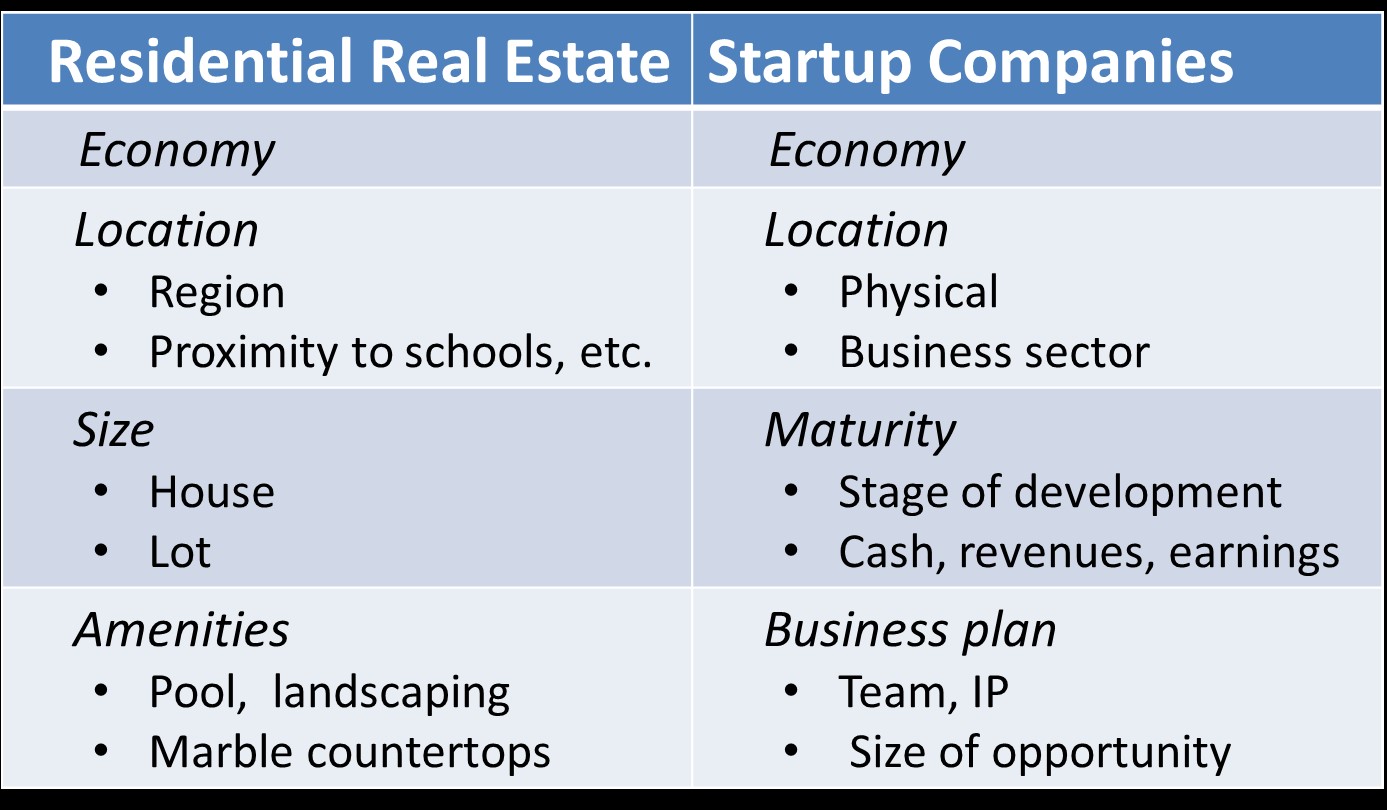

Monday, March 16, 2015 Monday, March 16, 2015 Why Does Startup Pricing Vary by Location?By: Bill Payne, Frontier Angels Entrepreneurs seem genuinely surprised to find that investors in Peoria or Little Rock are not willing to invest in startup companies at Silicon Valley prices. After all, they just read in TechCrunch that investors funded a company similar to theirs at an $8 million pre-money valuation! The valuation of startup companies shouldn’t be impacted by location, should they? Guess again! A newly-constructed 3500 square foot home with a pool near New York City is priced well above a similar home in Fargo, right? Well, the same differentials are true for startup companies. In fact, the issues that influence residential real estate pricing are quite analogous to those which determine the price investors will pay for ownership in startup companies. We know that investors will invest in hot startups run by celebrity serial entrepreneurs at much higher pricing than for similar startups with first-time entrepreneurs. And, we’ve heard that life science startups are often priced well-above software startups. But, what other factors impact startup valuation? Economy The real estate market fluctuates wildly with the economic cycle. Homes in Las Vegas that sold for $1 million in 2006, could only command prices of $400-500,000 in 2010. By 2015, many of those homes had regained much of their value from the peak in the economic cycle in 2006. The same is true for software/Internet companies. Investors who funded those companies for $1 million pre-money valuation in 2010 saw pricing for similar ventures soar to $4 million by 2015. Both markets are impacted by the economy. Buyers are scarce for residential real estate at the bottom of the economic cycle and the same is true for startups. Investor sources dry up in poor economic times. In down markets, entrepreneurs seeking capital must sell larger percentages of ownership in their startup companies to raise capital. Location, location, location…. Yes, residences located in competitive regions, such as New York City versus those in less competitive markets, such as Missoula, command higher pricing for similar homes. And, within a region, residences in the best neighborhoods and near highest quality schools are priced higher than elsewhere in the same region. The analogy is true for startups in Palo Alto versus those located in Kansas City. Demand is simply higher in some regions than others. So, pricing will be higher where larger numbers of investors are chasing interesting deals than in those markets with limited capital sources. In fact, within a region, capital intensive startups often command higher pricing that others which require less capital to achieve first revenues, because investors recognize that more resources may be required for capital intensive ventures to meet sufficient milestones to become fundable. Size and Maturity In my analogy (see table below), I have chosen to compare the size of a residence (both square footage of the home and lot size) to the maturity of the venture. Larger houses are priced higher than similar but smaller homes located nearby. Likewise, startups without a proven track record are priced below those with companies with revenues and earnings in similar markets. Other factors being similar, later stage companies are priced well above those with little customer validation and no earnings history. Analogy: Comparing Factors Impacting Values of Residential Real Estate to Startup Companies

The Business Plan The fourth comparison is of the amenities of a residence to those of a startup company. Homes with pools, dramatic décor and gorgeous landscaping sell at higher prices per square foot than their not-so-attractive, yet nearby neighbors. The same is true for new companies. Startups with an awesome, experienced team, quality intellectual property and a fractured yet huge marketplace are priced above those with less experienced teams with some IP and smaller opportunities. Bubbles There is one more similarity between residential real estate and startup pricing: irrational exuberance. In 2006, real estate buyers in Las Vegas somehow believed that skyrocketing pricing would continue indefinitely, prompting senseless speculation. Pricing promptly dropped as much as 50 percent in following years. Historically, real estate price inflation has reoccurred regularly. We see analogous bubble pricing in startups. Investors drove pricing way too high in 1999-2000, again in 2006-7 and perhaps again in 2015. When pricing is too high, entrepreneurs often raise too much money and lose their sense of lean operations, spending money unnecessarily. Inflated startup investment leads to down rounds, excessive dilution of entrepreneurs and investors and reduced returns to both. Have we entered another of bloated pricing of startups? Only time will tell. Summary Entrepreneurs are often told that the team, the product and the plan are the only significant considerations in determining the pre-money valuation of their startup company. Yes, these are important considerations, but only within a range of pricing which is determined by the economy, their location in this country and the maturity of their venture. The high tech press, mostly located in Silicon Valley, reports on venture pricing for deals financed in Silicon Valley, which cannot be assumed to be consistent across the country. A startup venture can only be priced with a good understanding of the financial cycle and the competitiveness for startup financing in the region of the venture. As with real estate, location…location…location is the abiding factor in defining the range of pre-money valuations for startup companies. The clear message is that you should pay close attention to the pricing of similar startup ventures in your neighborhood. And, if you sense we have entered another bubble of inflated pricing, perhaps it is time for investors to be more selective in their angel investing. |

Comments