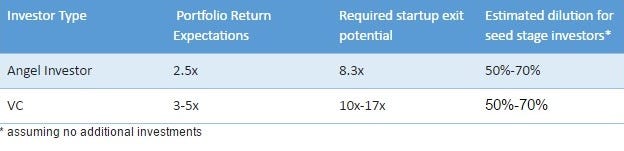

Monday, September 19, 2016 Monday, September 19, 2016 What’s the Real Value of a Startup?By: Swati Chaturvedi, Medium/ @propel(x) This blog initially appeared on Dissected by propel(x) blog on Medium. It shows how one angel investor thinks about valuations. Other angels may have different thoughts or calculations, but it is a resource for entrepreneurs to learn about the equity raising process. Putting a value on your visionary idea — you know, the one that’s going to change the world — can be tricky. To you as a founder, your idea is priceless. To investors…not so much. In reality, it’s investors’ job to think about it differently and press down on valuation. Understanding their perspective with regard to valuation will help your fundraising efforts go smoothly and net you the investments you’re after. So, how can startups bridge the gap between the investors’ thought process and theirs? A good place to start is by understanding how angels and VCs think about valuation and their portfolio as a whole. Then, startups should consider some basic data and work backwards to arrive at an implied valuation. First, some math! Let’s start with how angel investors set their expectations and think about valuation (or how they should think about valuation.) Angel investors have had a ~2.5x exit on average when investing in startups according to the Angel Resource Institute. Holding periods for successful exits are in the 4.5 year range. And angel investors should expect 50%-70% dilution when investing at the seed stage.

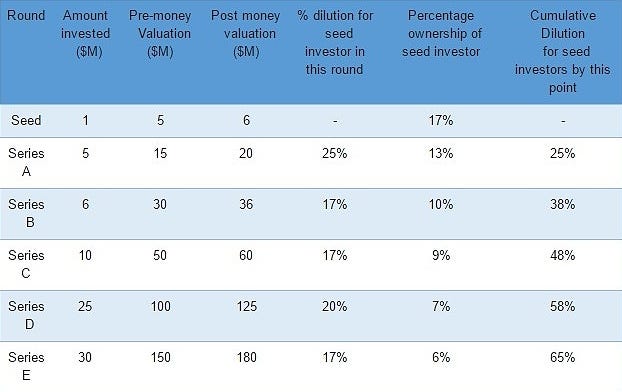

Here is a simplified example of how valuations might progress through the life of the company, along with expected dilution for seed investors that invest an initial $1M (assuming all goes well): Based on the numbers above, if the exit happens after Series C, a seed investor would expect to be cumulatively diluted by about 50%; if it happens after Series E, the investor is diluted by about 65%. In general, investors expect a 50%-70% dilution. If the exit after Series C is in the ~$70M range, the seed investor would get ~9% of the proceeds, or $6.3M. That is a great outcome; 6.3x the initial investment. If this occurs within a reasonable time frame, the rate of return is high as well (36% Internal Rate of Return (IRR)if an exit occurs in the 7th year after investment). But this is an example where all goes well, valuations steadily rise, and a return is delivered as promised. In most cases however, all does not go well. There are down rounds, longer timelines, greater than expected dilution, and capital losses. As a result, overall the portfolio return has been in the 2.5x range versus the 6.3x shown in the rosy scenario above. Considerations for the startup: With this in mind, here’s what a startup should be considering: Since most investors expect ~50–70% dilution, at the time of investment, a startup should carry the promise of at least 8.3x exit multiple [=2.5x/(1–70%], so that on average, after capital losses, investors end up with a 2.5x return on their portfolio. In other words, if the valuation at the time of investment is $10M, the startup should have the potential to be sold at $83M (8.3x initial valuation); If initial valuation is $5M, exit potential needs to be at least $42M…and so on. For venture capital, the required exit potential grows significantly — most VCs are looking to return 3x-5x of investor capital. Therefore, if they invest at the seed stage, the required multiples should be in the range of 10x-17x.

Expectations and Valuation:

Startups should simply work backwards from the above; set valuations based on expected exit. If expected exit is $42M, set a valuation of $5M (=42/8.3); if expected exit is $80M+, set a valuation of $10M…you get the picture. So far so good? Not so fast. . . Let’s get real: Here is where reality intrudes. How do you know what the ‘expected exit’ is? To arrive at an ‘expected exit’ value, startups (and investors) need to study the industry and exit trends overall. Find out what the exits have been historically and recently. The average of these is a good proxy for your expected exit. An added wrinkle is that some startups create new markets — so there are no good proxies. Sadly, that is the life of startups and investors — they need to live with ambiguity! The disconnect between startups and investors happens when startups are not able to demonstrate an exit potential that is in line with the initial valuation. For example, the startup expects an initial valuation of $10M, while exits in that particular industry have only been in the range of $50M-$70M or 5x-7x — which is less than the desired exit potential. If your seed stage valuation is $10M, you need to show industry exits in the range of $80M-$100M. This is already difficult — exits in the $100M+ range are rare. It only gets harder as the initial seed stage valuation rises. To bridge this gap, startups need to do two things:

Understanding the perspectives of investors will put your startup in a great position as you come up with your valuation. Get data on similar exits, find proxies, share data with investors, and help them understand what return they will get if you execute as promised. Work out the math for them and show them your process. And with that you will have a winning fundraising formula that sets your company up for success. Tags: |