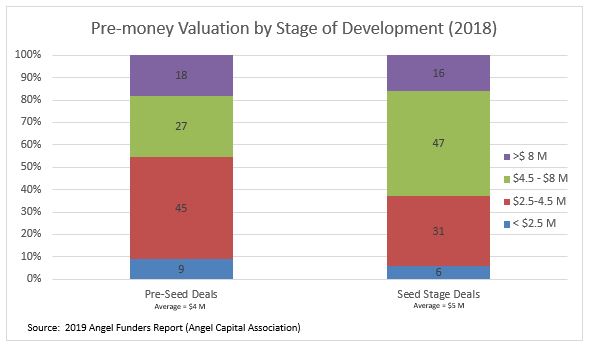

Monday, October 21, 2019 Monday, October 21, 2019 Scorecard Valuation Methodology (Rev 2019): Establishing the Valuation of Pre-revenue, Start-up CompaniesBy: Bill Payne, Frontier Angels This article was originally written in May 2001 and has been updated multiple times. Others have referred to this and similar methods as the Benchmark Method and the Bill Payne Method. The Scorecard Valuation Methodology is useful for investment in most pre-seed and seed stage opportunities, except those with very high capital requirements prior to achieving first revenues (such as some life science and energy deals). Background Individual accredited investors in typical angel deals put personal capital at risk for an equity share1 of growth-oriented, start-up companies. These angel investors generally invest $25,000 to $100,0002 in a round totaling $250,000 to $1,000,000. In 2018, the valuation of pre-revenue, start-up companies is typically in the range of $3 to $8 million and is established by negotiations between the entrepreneur and the angel investors. For this round of investment, the angels collectively purchase 10-30% of the equity of the company and are seeking a return on investment of 10-30X in a period of five to ten years. Active angels invest in a diversified portfolio of at least 10 companies, usually spreading their investments over a few years. Experience proves that half of these companies will fail (returning nothing or less than capital invested), another 3-4 will provide a modest return on investment of 1X to 5X, and one or hopefully two of the ten companies will return 10X to 30X on the initial investment over a five to ten year period of time. In the end, such a portfolio might yield the angel investor a total return on investment of 20% per year or more. These anticipated outcomes first reported by Wiltbank’s “Returns to Angels in Groups” in November 2007 have since been validated by several angel groups in the US. Angels typically invest in companies operating in industry sectors with which they are familiar. Diversification across industry sectors is not as easily achieved for angels as could be accomplished in public markets, but can be achieved by co-investing with trusted angel colleagues in a broader set of businesses. A local affiliation of angels can be important to achieving a diversified portfolio. Working within a group of angel investors also expands the pool of expert resources and helps divide the work of screening companies and investment due diligence. Furthermore, angel groups frequently syndicate (co-invest) with other trusted angel organizations in an effort to help fill round of investment for local companies and assist members in diversifying their portfolios of angel investments. To achieve a satisfactory return on investment, for every ten investments in an angel’s portfolio, one or two companies must return 10–30X on the initial investment. It is, of course, impossible to predict at the outset which of these portfolio companies will be successful and which will fail. It is necessary, then, that each investment in the angel 1 A significant fraction of pre-seed and seed stage deals are done as convertible debt. In such deals, this method is useful in determining the cap on the note, that is, the maximum valuation at which the notes will later be converted into equity. 2 Some angels invest as part of an angel or seed fund. Angels in angel funds invest their pro-rata share of the fund in each deal done. portfolio demonstrates the potential to scale sufficiently to provide a 10-30X return on investment. Due to the high failure rate in startup companies, including a substantial number of investments with lesser growth opportunities in an angel investor’s portfolio only reduces the possible return on the entire portfolio. Scorecard Valuation Methodology This method compares the target company to typical angel-funded startup ventures and adjusts the median valuation of recently funded companies in the region to establish a pre-money valuation of the target. Such comparisons can only be made for companies at the same stage of development, in this case, for pre-revenue (or minimal revenue) startup ventures. The first step in using the Scorecard Method is to determine the median pre-money valuation3 of pre-revenue companies in the region and business sector of the target company. Pre-money valuation varies by geography within the US economy and with the competitive environment for startup ventures within a region. In most regions, the pre-money valuation does not vary significantly from one business sector to another4. If insufficient local data is available, angels can refer to recent national studies published by the Angel Capital Association in the “Angel Funders Report,” as is shown below:

3 Pre-money valuation is the value of a startup enterprise just before investment. Post-money valuation is the value of this enterprise just after investment. Hence: pre-money valuation + investment = post-money valuation. 4 As mentioned above, some startups in life science and other sectors required huge amount of capital to finalize revenue generation. For these companies, the Scorecard Method may be less useful. For purposes of this report, let’s assume the midpoint between the average Pre-Seed Deal ($4M) and Seed Stage Deal ($5M) is an appropriate median local pre-money valuation, that is, $4.5 million (our starting point for this example). The Scorecard Method then adjusts this starting point by considering the strengths and weaknesses of the target startup. The next step in determining the pre-money valuation of pre-revenue companies using the Scorecard Method is to compare the target company to your perception of similar deals done in your region, considering the following factors: Strength of the Management Team 0-30% Size of the Opportunity 0-25% Product/Technology 0-15% Competitive Environment 0-10% Marketing/Sales Channels/Partnerships 0-10% Need for Additional Investment 0 - 5% Other 0 - 5%

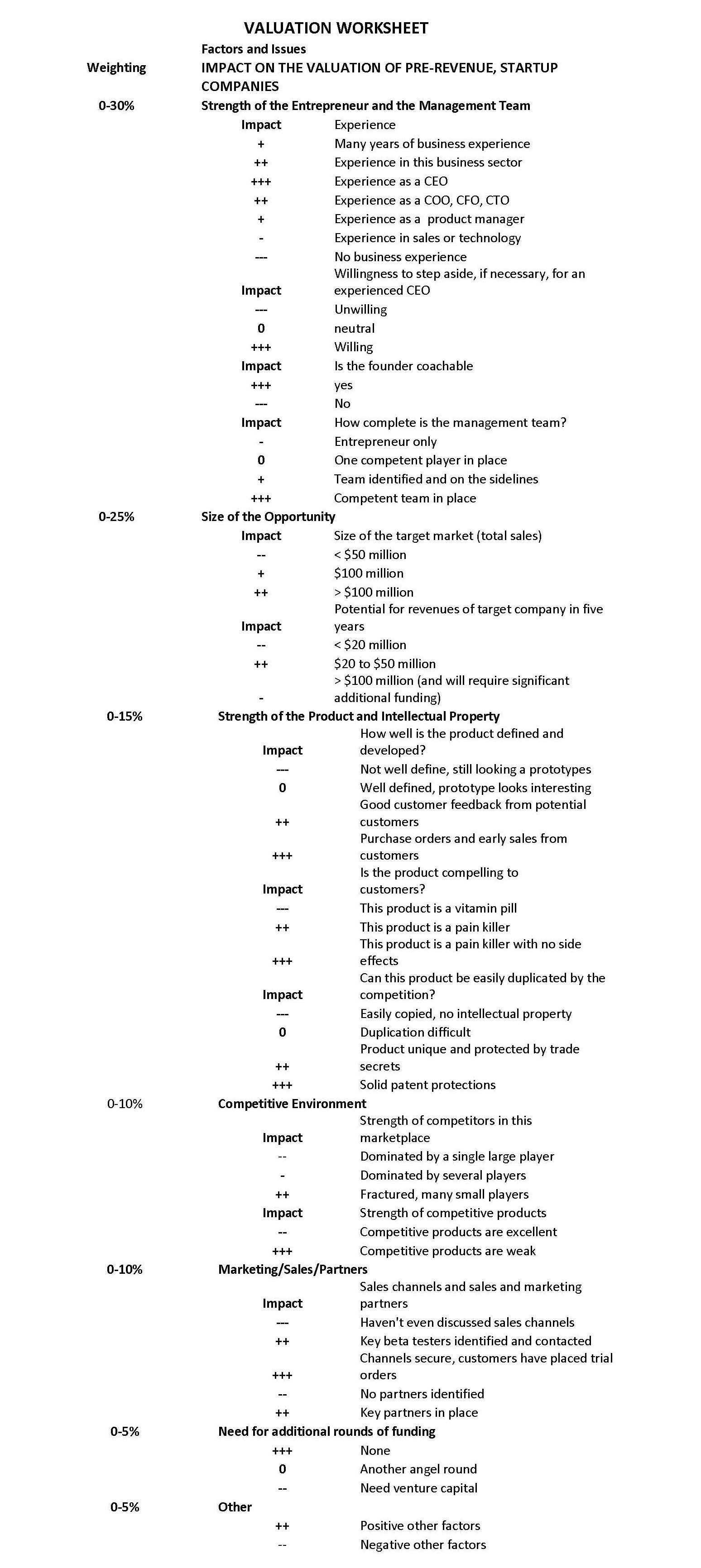

A Valuation Worksheet is provided in the appendix to this document to assist readers in judging the relative strength of target companies for the above categories. The subjective ranking of factors (above) is typical for investor appraisal of startup ventures. Some are surprised to find that investor rankings of product and technology are below those of the management team and the size of the opportunity. In building a business, the quality of the team is paramount to success. A great team will fix early product flaws, but the reverse is not true. And, as has been discussed earlier, scalability is critical to investor returns. Good product and intellectual property are important, but the quality of the team is key. Making the Valuation CalculationTo provide an example, assume a company with an average product and technology (100% of norm), a strong team (125% of norm) and a large market opportunity (150% of norm). The company can get to positive cash flow with a single angel round of investment (100% of norm). Looking at the strength of the competition in the market, the target is weaker (75% of norm) but early customer feedback on the product is excellent (Other = 100%). The company needs some additional work on building sales channels and partnerships (80% of norm). Using this data, we can complete the following calculation: COMPARISON FACTOR RANGE TARGET COMPANY FACTOR Strength of Entrepreneur and Team 30% max 125% 0.3750 Size of the Opportunity 25% max 150% 0.3750 Product/Technology 15% max 100% 0.1500 Competitive Environment 10% max 75% 0.0750 Marketing/Sales/Partnerships 10% max 80% 0.0800 Need for Additional Investment 5% max 100% 0.0500 Other factors (great early customer feedback) 5% max 100% 0.0500 Sum 1.1550 Multiplying the Sum of Factors (1.155) times the median pre-money valuation of $4.5 million (the appropriate median local pre-money valuation discussed above), we arrive at a pre-money valuation for the target company of just over $5.2 million. Summary Key to the Scorecard Method is a good understanding of the median (and range) of pre-money valuation of pre-revenue companies in a region. With this data in hand, the Scorecard Method gives angels subjective techniques to adjust the median valuation of local startups in similar business sectors to arrive at a pre-money valuation for a target seed stage company. Savvy entrepreneurs can use these tools to prepare for negotiations of valuation with investors. Appendix to Scorecard Valuation Methodology Armed with median and range of pre-money valuations for pre-revenue, start-up companies in the region, what determines where in that range is a fair valuation for a specific company? The worksheet below is an empirical Valuation Worksheet. This worksheet will not provide the investor with a neat and tidy dollar valuation for a pre-revenue, start-up company! This worksheet provides the investor with a basis for deciding if a start-up company should be valued near the top or bottom of the range of values that might reasonably be applied to such an early stage venture. The worksheet is a listing of issues and factors that should be considered in judging the value of a company. Note the following features of the worksheet:

No two angel investors will value a company (or business plan) the same, however, with some practice, this worksheet will allow investors to compare one company to the next and assist angels in deciding if a company’s valuation should be near the high end of a reasonable range in valuation or, on the other hand, near the bottom of the range of valuations.

Tags: |