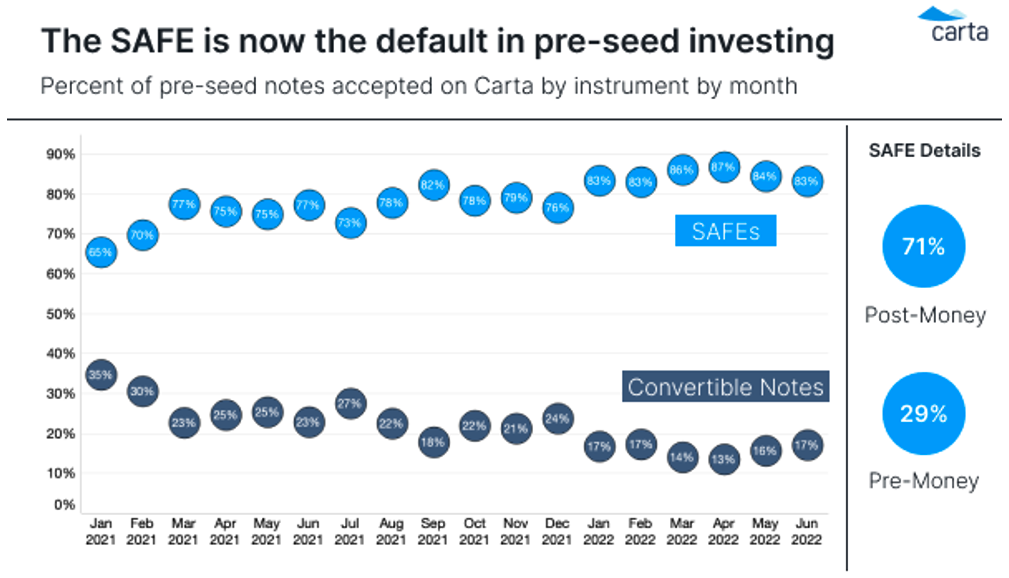

SAFEs! They’re apparently everywhere. And it is easy to understand why this perception persists. Y Combinator, a leading incubator, invented the original (pre-money) SAFE (Simple Agreement for Future Equity) in 2013 to provide an easy, fast and cheap way to fund the dozens of startups comprising a Y/C batch. Their rationale was simple. Companies receiving small amounts of cash should not spend much of that on legal fees or waste time negotiating complex legal terms so early in a startup’s journey. As Carta indicates, the SAFE has become the “default” for earliest stage deals:

FIGURE 1: PERCENT OF SAFES AS PRE-SEED NOTES ON CARTA

But the SAFE note quickly escaped, COVID-like, from the pre-Seed incubator lab to the general startup population, and not just for the earliest deals. Y/C helped enable this by introducing the Post-Money SAFE in 2018, fixing some of the more egregious problems with SAFEs, principally the lack of transparency about valuations when multiple SAFEs convert to equity. The Post-Money SAFE, by design, made it easier for SAFEs to be used in larger financing rounds and has largely replaced the original SAFE.

Startup CEOs love SAFEs, not simply for their simplicity and low cost, but also because the original SAFE’s terms tilted the balance of power sharply towards CEOs against investors. At the same time, the Post-Money SAFE’s emphasis on valuation transparency brought a bit more balance to that relationship. But serious problems remain, particularly the exclusion of investors from having governance rights or roles. Since Y Combinator plays an outsized role in the life of their portfolio companies, it didn’t need many of those priced round protective and governance provisions to ensure a dominant role in the next stage of a portfolio company’s journey. Lawyers, too, love SAFEs. Executing a SAFE requires very little work as there is very little to decide, negotiate or explain.

So, are SAFEs truly dominating early-stage investing? Such is the common perception. But what about angels? What is the role of SAFEs in our deals? To answer this question, let’s first identify the stage at which angels most commonly invest.

Whomever is doing the bulk of those pre-seed deals examined by CARTA, it is probably not America’s leading professional angel groups. FIGURE 2, drawn from the ACA’s Angel Funders’ Report database, examines the funding rounds in which angel groups participated between 2019 (the year after the Post-Money SAFE was introduced) and 2021. FIGURE 2 indicates that pre-seed deals accounted for only 4% to 5% of all ACA angel group rounds. In contrast, Seed and Series A collectively comprised 70% to 80% of ACA angel rounds, with Seed stage, by itself, accounting for nearly 50%. Seed is clearly the most popular stage at which angel groups invest:

FIGURE 2: ANGEL GROUP ROUNDS (2019-2021)

Source: ACA Angel Funder’s Report Database

Pre-Seed, which CARTA has demonstrated is dominated by SAFEs, accounts for only a tiny fraction of ACA angel group deals.

So, what about Seed Stage, the angel’s most frequent investing stage? Is it also dominated by SAFEs? FIGURE 3 examines the different types of securities used at each stage at which ACA angel groups invested from 2019 through 2021. For all stages of angel rounds the percentage of SAFEs increased from 3.5% in 2019 to 8% in 2020, and remained at that level in 2021.

Examining deals by stage, for pre-Seed, SAFEs more than doubled in frequency between 2019 and 2020, jumping from 10% to 28% of all pre-Seed deals done by ACA angel groups. However, by Seed stage, the percentage of SAFEs declined by nearly 60%, from 28% at pre-Seed to roughly 12% at Seed stage in 2020 and 2021. Seed stage angels decisively preferred traditional priced equity and convertible notes, which comprised approximately 85% of all Seed deals. And it was traditional preferred equity that dominated Seed deal structures, accounting for nearly 50% of all deals in both 2020 and 2021. And, of course, Series A and later stages were decisively dominated by preferred equity deal terms.

FIGURE 3: DEAL STRUCTURES BY TYPE OF ROUND (2019 – 2021)

Source: Angel Funder’s Report Database

As CARTA has demonstrated, it is undeniable that SAFEs have made a major impact on pre-Seed funding, though less so (according to ACA data) when angel groups participated in those pre-Seed rounds. SAFEs remain prevalent for incubator and earliest stage startup hub deals, stages typically prior to major angel investing.

But when it comes to deals done by sophisticated angel groups, for whom protective provisions and mature governance really matter, SAFEs have not made much of an impact, amounting to less than 10% of deals at all stages in 2021. And remember that 2021 was the most management-friendly deal year, with the highest valuations on record. Another reason for the preference for priced rounds is that these rounds clearly start the clock on the holding period for QSBS favorable tax treatment.

FIGURE 4: % OF ANGEL DEALS BY DEAL STRUCTURE

Source: Angel Funder’s Report, 2022

Key Takeaways:

- For earliest stage deals, when little is known and complex deal structures are less relevant, SAFEs offer speed, simplicity and low cost.

- By the time companies need to raise a true Seed stage angel round, they often have to deal with more complex investor, employee, partner, customer, competitor and IP matters. Experienced angels know that these issues call for more sophisticated deal terms. Convertibles and Priced Equity deals give both investors and management greater protections and clearer visibility.

- And governance really starts to matter at Seed stage. This has recently and amply been demonstrated by the reappearance of Boards and serious governance as critical deal terms. Good governance promotes more resilient startups by being better able to deal with today’s tougher financial and operational challenges.

Author:

- Ronald Weissman, Band of Angels and Vice Chair, Angel Capital Association