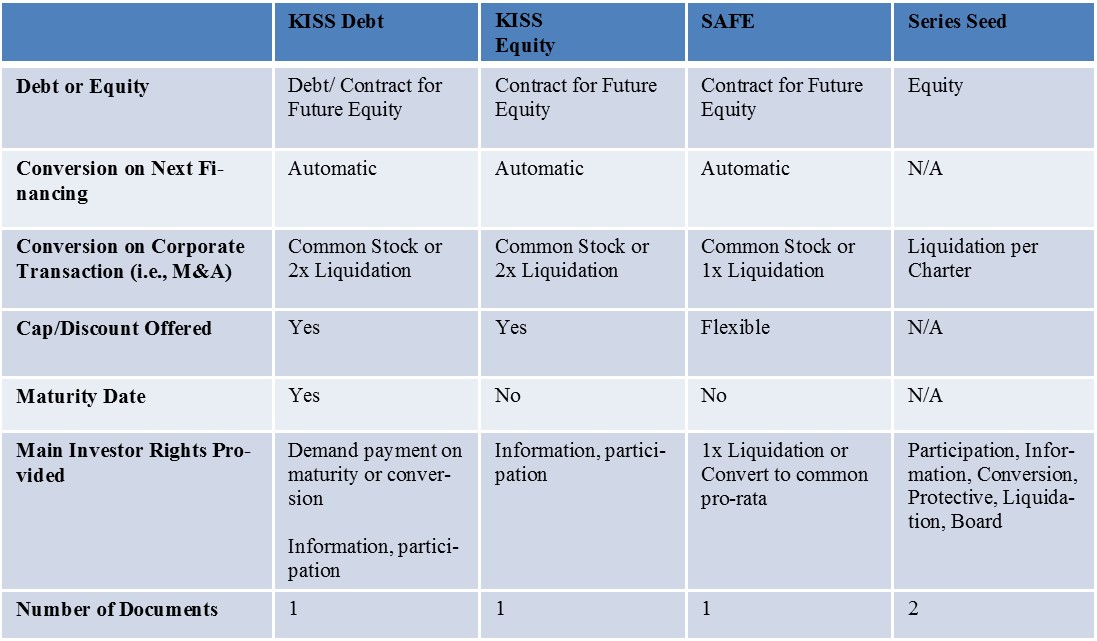

Wednesday, April 29, 2015 Wednesday, April 29, 2015 Revisiting Early-Stage Investing VehiclesBy Michelle Stewart and George Willman, of Reed Smith LLP Traditionally, investors have selected between two main modes of accomplishing early-stage financing – direct issuance of equity or convertible debt. There have been some changes over time, such as the increasing proportion of early-stage financings using convertible notes, and increased investor demand for better economics in the notes, with features such as valuation caps and discounts to conversion. However, for a long time, early-stage investments were generally limited to these two modes of financing without a lot of fundamental change. Recently, several new approaches have emerged, which have generated quite a bit of interest in the early-stage financing community. These include SAFE (Simple Agreement for Future Equity), KISS (Keep it Simple Security), and Series Seed. SAFE, proposed by Y Combinator, and KISS, proposed by 500 Startups, were quickly adopted by companies coming out of these well-known accelerators. But the use of, and interest in, these new approaches reaches beyond these portfolio companies to other emerging companies looking for something different. The Wall Street Journal highlighted this trend recently in “Startups Offer Unusual Reward for Investing - Simple Agreement for Future Equity promises benefits later if the firm is able to move forward,” April 1, 2015. Entrepreneurs are drawn to these new approaches particularly by the prospect of saving cost and time. Notably, SAFE and KISS are each a single document, as opposed to the several documents required for a preferred stock financing (stock purchase agreement, investor rights agreement, voting agreement, amended certificate of incorporation, etc.). Though popular with entrepreneurs, investors have not embraced the new approaches universally. There are tradeoffs among the various new approaches and as compared with traditional financings. Some of the key terms are highlighted in the chart below:

SAFE is similar to convertible debt in several of its features. Unlike convertible debt, SAFE lacks a maturity date. To some extent, a maturity date is irrelevant because an early-stage investor often invests for upside, realized through the conversion into equity in a successful company, not to be simply paid back on maturity with interest. However, some investors feel that the maturity date is an important right, particularly when the convertible debt otherwise lacks a number of the rights of an equity investment. Companies should keep in mind that while these new instruments may be cheaper and quicker to put in place than a fully negotiated traditional preferred stock financing, there can be added complexities when the time comes to actually convert these new instruments to equity in the company. One example of this is demonstrated when investors in the next round are negotiating their rights, and a debate arises as to whether the holders of these new instruments should receive all of the rights and preferences of the new round. Although there are solutions to address some of the concerns (e.g., “shadow preferred” stock), these come with added complexity and can take time to negotiate. Series Seed is most like a traditional preferred stock financing but is simpler. However, given its similarity to a traditional preferred stock financing (e.g., Series A), the Series Seed may not result in much of a costs savings – its popularity may be driven by the company’s desire to not label a financing “Series A” too early and instead wait until it is ready to approach the venture investors. Only time will tell to what extent these instruments supplant the more tradition modes of early-stage financing. In the meantime, both companies and investors should carefully weigh the tradeoffs of costs, speed, rights and complexity.

Reed Smith represents many of the world's leading companies in complex litigation and other high-stakes disputes, cross-border and other strategic transactions, and crucial regulatory matters. With lawyers from coast-to-coast in the United States, as well as in Europe, Asia and the Middle East, Reed Smith is known for its experience across a broad array of industry sectors. Reed Smith counsels 13 of the world's 15 largest commercial and savings banks; 25 of the world's 35 largest oil and gas companies; and the world's three largest pharmaceutical distribution and wholesale companies. Reed Smith's shipping practice has been designated among the most preeminent in the world, and its advertising law practice is regarded as among the legal industry's finest. |

Comments