This is Part 2 of a two-part examination of the state of the startup capital market during the past two years. For Part 1 on The Equity Seller’s Bubble of 2021, click here to access the ACA Data Insights Archive.

2022: The Aftermath

In 2022 war, inflation, rising interest rates and a tougher economic environment–one not buoyed by historically low interest rates–brought an end to the long-term bull market in assets (the “everything bubble”), including startup capital. From an investor’s perspective, 2022 witnessed a sudden market reversal from an extreme equity seller’s market to an equity buyer’s market, causing dislocations throughout angel, VC, and startup ecosystems. This transformation has already led to an increased number of startup failures, a growing venture capital reset2 and 210,000 tech sector layoffs since the start of 2022.

2A (temporary) venture capital reset? Major capital market disruptions often bring a “VC Reset,” as venture firms rethink fundamentals, often pressured to do so by limited partners. As many angel funds are modelled on standard venture practice and as VCs are often the “next check” after ours, we need to be alert to these issues:

- Tougher terms from limited partners for all but the historically best performing top 30 funds and a much tougher fundraising climate for new VCs. Some limited Partners have requested lower fees (1.5% rather than 2%), elimination of bubble economics (like 25%+ carried interest for some top funds) and other LP-friendly terms. It is unclear if VCs will agree to these terms, but LPs believe they now have more leverage. In 2022 VC fundraising remained strong but a greater share of dollars went to a smaller number of firms.

- Greater governance role for limited partner Boards of Advisors.

- A growing awareness that VCs need staff having a broader range of experience and backgrounds.

- An awareness that diligence needs to be tougher and less trusting, particularly after the FTX debacle. A much contested University of Chicago report suggested that contemporary diligence practices are flawed and that 50% of VC bets are “predictably bad.”

- A shift from late-stage pre-IPO investing to renewed emphasis on early stage. On the one hand, there will be more investors to write follow-on checks for our deals; on the other hand, top-tier VCs are launching $400M – $500M seed funds accompanied by larger value-added portfolio support staff, providing more deal competition.

- From VCs to Investment Advisors… and back again? Several top-tier funds recently redefined themselves as “investment advisors,” enabling them to place long-term bets by holding rather than distributing IPO shares. The rapid decline of public market valuations right after VCs made this shift may dent the enthusiasm for this trend.

- Higher litigation risks. The SEC is considering rules making it easier for limited partners to sue venture firms for negligence and weak diligence. All asset managers, not just VCs, would be subject to this greater risk. But this will be especially hard to deal with for early-stage investors, given that we expect most of our investments to fail to return capital. Will normal and inescapable business risks now be subject to greater liability?

- Smaller VC fundraises? For the near future, investors in venture funds will likely see fewer and less valuable exits. A reduction in returns might lead investors in all but the top funds to reduce their commitment to future funds at least until a broad market recovery. This could reduce the supply of startup capital near term.

VC resets are often short-lived. After the Great Recession, the Kauffman Foundation issued a blistering report on the state of venture “We Have Met the Enemy And He Is Us: Lessons from Twenty Years of the Kauffman Foundation’s Investments in Venture Capital Funds and the Triumph of Hope Over Experience,” Kauffman Foundation, 2012. Within five years, with the return of an active IPO market, the practices of which the Kauffman Foundation complained had returned in force as hope, again, triumphed over experience.

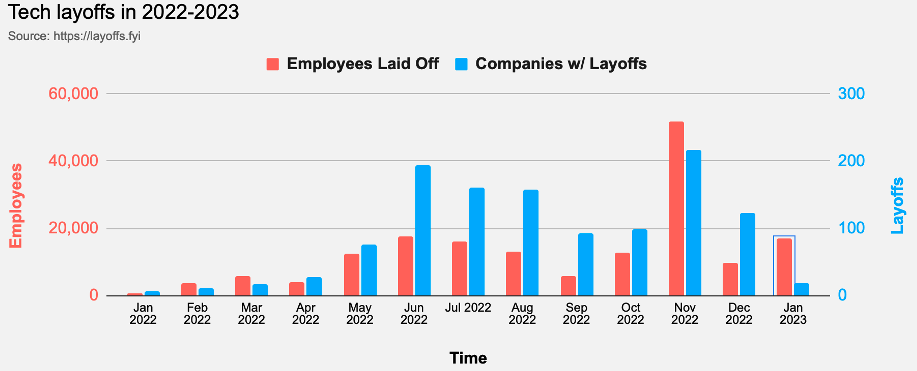

FIGURE 10: US TECH LAYOFFS SINCE 1/1/2022

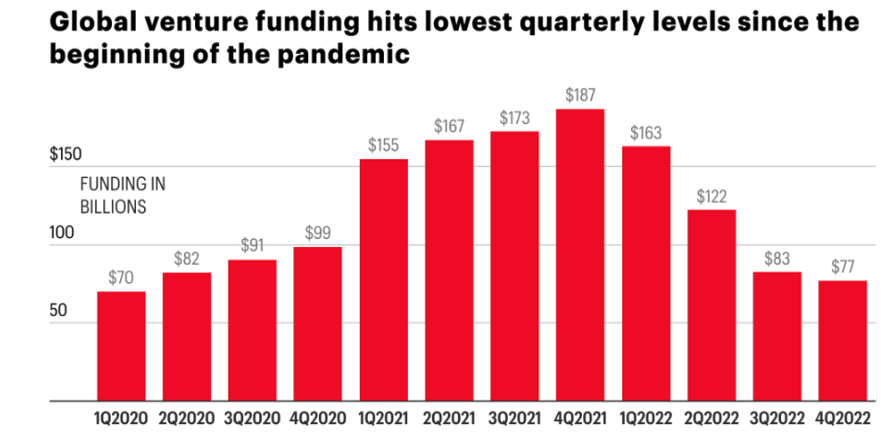

FIGURE 11: QUARTERLY GLOBAL VC INVESTMENTS, Q1 2021 – Q4 2022

The 2022 decline in funding hit almost every geography:

FIGURE 12: 2021 VS. 2022 GLOBAL FUNDING

Source: CB Insights Data Aggregated By R. Weissman

In the US, public market valuations dropped by 50% or more in virtually all industry sectors, affecting the comparables generally used by angels and VCs to value revenue-stage companies:

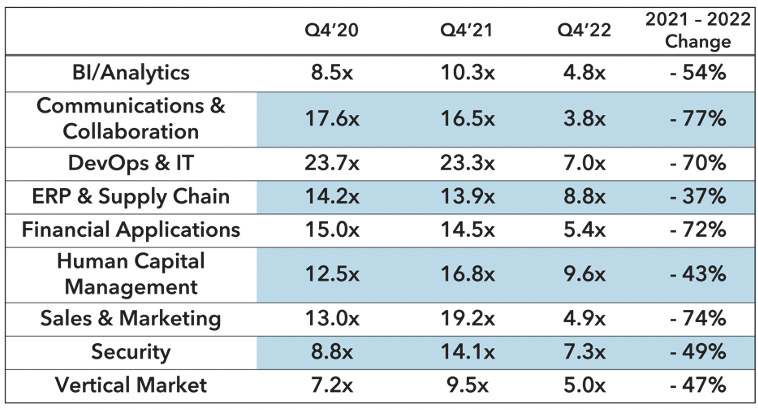

FIGURE 13: Q3 2022 VS. Q3 2021 PUBLIC MARKET MULTIPLES FOR SAAS SECTORS

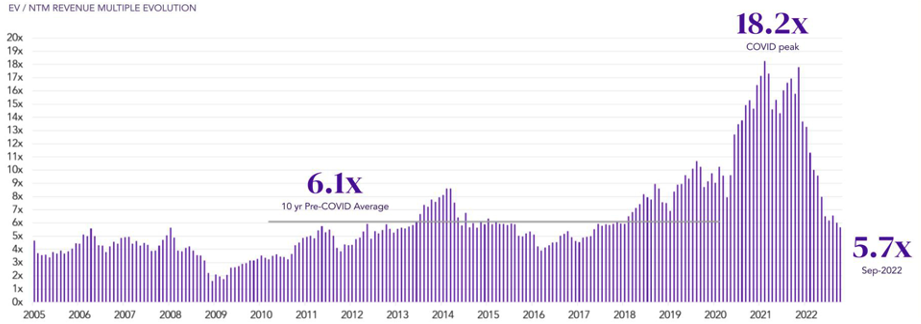

Globally, by 2021 median revenue multiples (US, EU, Israel combined) had grown three times the previous ten year period of relatively stable values from 6.1x to 18.2x. In a sharp reversal of 2021 values, 2022 SaaS multiples declined by more than two-thirds, returning to their 2019 levels.

FIGURE 14: EU/US/ISRAELI SAAS MULTIPLES

As we have seen, later stage valuations increased the most and early stage, the least during 2020-2021. The 2022 correction has followed the same path. The faster the rise, the harder the fall. The most inflated 2021 valuations and deal volumes (late-stage) saw the sharpest declines in 2022. As in previous bubble deflations, the malaise began with public market declines—a sharp Q1’22 fall in the S&P 500 — and successively impacted unicorns and other pre-IPO companies, then late/growth stage and finally early-stage and seed-stage/angel investing.

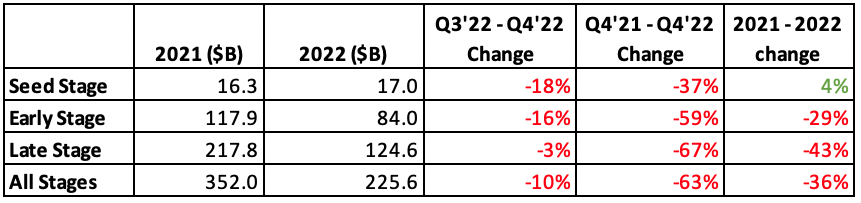

FIGURE 15: 2021 VS. 2022 US STARTUP FUNDING BY STAGE ($B)

Source: R Weissman Aggregated Crunchbase Data

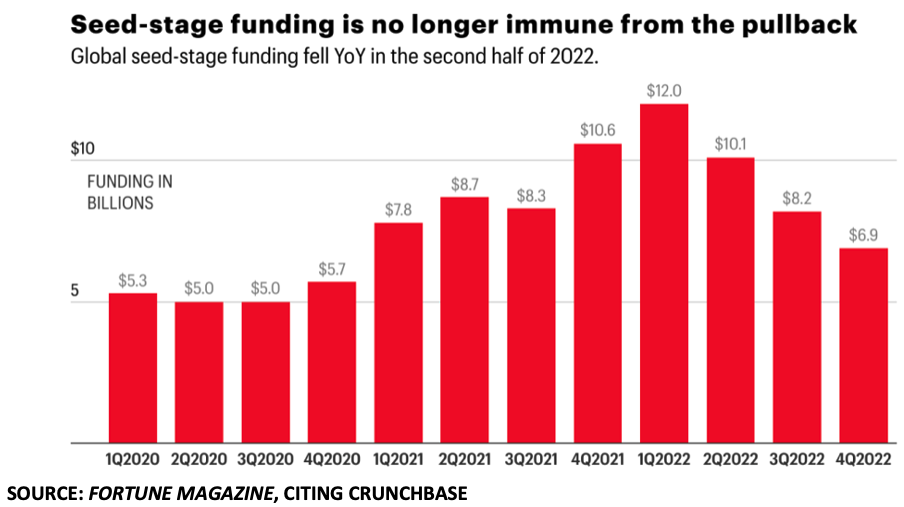

Overall, annual venture funding fell by 36% between 2021 and 2022. Early and late-stage funding had already decreased by mid-year, followed by further but modest decreases from Q3 to Q4. Seed stage remained the most resilient at the beginning of 2022 but later in the year saw a funding decline, culminating in Q4 with a 37% US decrease (compared to Q4’21) and a 35% decline globally. Nevertheless, seed stage funding remained more resilient than other stages.

FIGURE 16: GLOBAL SEED STAGE FUNDING, Q1 2020 – Q4 2022)

Source: Fortune Magazine, Citing Crunchbase

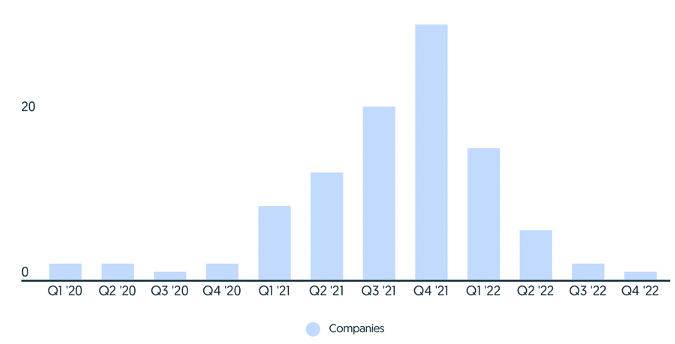

Funding is becoming harder to find at all stages. The outlook for Series Seed startups raising Series A is tougher than it has been but is still stronger than for companies raising later stage capital. Even more than a “Series A Crunch,” investors should be concerned about a potential Series B Crunch, too.

FIGURE 17: NUMBER OF COMPANIES ANNOUNCING NEW FINANCING ROUNDS

Source: Crunchbase

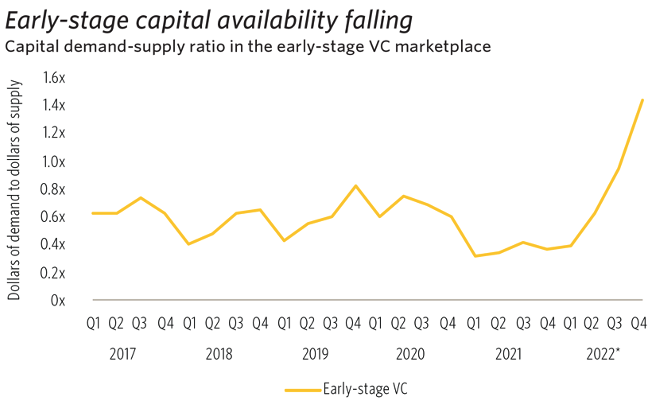

In 2022 the demand for capital outstripped the supply and this gap worsened as the year progressed. By Q4, for every dollar of available capital there were 1.4x dollars sought by startups, a rapid reversal of the 2021 ratio of capital supply to capital demand, a funding gap not seen since the “Series A Crunch” of 2013.

FIGURE 18: SUPPLY VS. DEMAND FOR EARLY-STAGE CAPITAL

Source: Pitchbook/NVCA MonitorFunding has dropped in most industry sectors year over year by as much as 30% to 60%, and the number of deals has declined, typically, in the range of 24% to 60%, depending on sector. Edtech has fallen the most; Healthcare, the least according to Pitchbook.

Private company valuations are influenced by public trading, IPO and M&A valuations, which offer a guide (however imperfect) to possible returns investors can expect. And as we’ve seen, public market valuations have declined over the course of 2022. High sector valuations used to justify funding in 2021 were followed in 2022 by public market valuations now 50% of those recent funding valuations.

50% drops in today’s public market valuations do not bode well for companies who raised funds at 2021’s inflated values. Those companies are now trying to justify or “grow” into their bubble valuations. Many of these companies have delayed raising capital in 2022 hoping for a market recovery in 2023. Many of the companies who raised funding in 2020/21 at abnormally high valuations are unlikely to see a return anytime soon to their bubble valuations of 2021.

A return to higher valuations is usually triggered by a stronger IPO market. When will today’s moribund IPO market recover? The 1987 downturn took three years to recover. The recovery following the Internet bubble collapse of 2000 similarly took three years. Recovery from the 2008 Great Recession took two years and was relatively weak. Few analysts are near-term optimistic about public markets, meaning that exit valuations may remain at 50% of recent values through 2023 or beyond, keeping comparables low, affecting every stage of fundraising and exit planning.

Capital market attorneys report that the IPO window remains closed for the most popular startup sectors. Companies who have filed to go public in 2023 are not emerging companies with tech metrics, but more mature companies in traditional industries with solid revenue growth and traditional business metrics: Oil and Gas, Industrial, Retail and Restaurants. (Law360, January 2, 2023). Attorneys also expect hundreds of SPAC failures as deadlines to find targets expire in early 2023.

Gone is the equity seller’s market of 2021. The deal balance of power has shifted towards investors. For 2023, we can expect longer deal cycles due to more extensive diligence, deals with more balanced founder/investor terms and more protective provisions, including higher liquidation preferences and stronger Board governance.

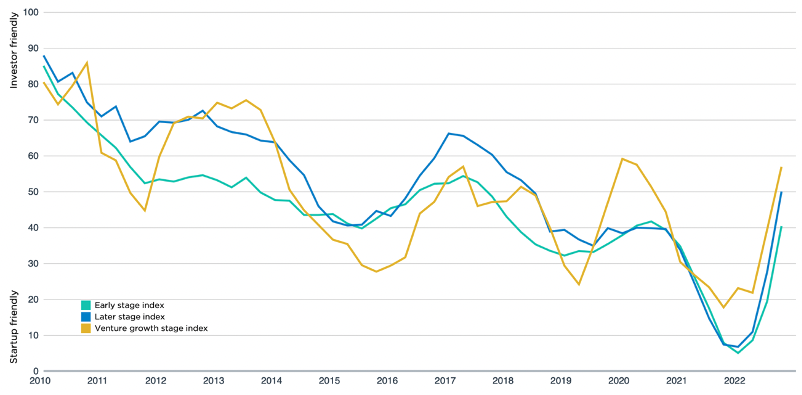

Illustrative here is Pitchbook’s VC Dealmaking Index, based on valuations, the relative supply and demand of private capital, the demand (or not) for board rights and related deal and environmental factors. Figure 19 (Pitchbook, January 4, 2023) charts the ebb and flow of founder vs. investor deal negotiating power. Pitchbook’s metric saw a sudden and sharp reversal from extreme founder-friendly (downward slope) to more investor-friendly (upward slope) deal climate in 2022.

FIGURE 19: VC DEALMAKING INDICATOR: FOUNDER FRIENDLY VS. INVESTOR FRIENDLY DEAL CLIMATE INDEX

Source: Pitchbook

The reversal of this index tracks similar reversals in deal volumes, dollars funded, and valuation trends. Today, all stages and most sectors are moving from equity seller to equity buyer markets. At the end of 2022, seed and early-stage deals (which had been relatively healthy during the first half of the year) began to decline, as well.

From investors to entrepreneurs and our ecosystem partners, the experience of the abnormal last several years is causing a global private capital reset, no longer business as usual, as we search for a “new normal.” But as with most crises, opportunities for experienced investors who have learned from prior down cycles are still plentiful.

Summary:

- 2021 saw the height of startup funding at the end of the longest bull market in recent history. 2021 Startup funding broke records for capital invested and for high valuations. It also saw the continued growth of SAFEs, the ultimate unbalanced, founder friendly and investor-hostile deal instrument.

- 2021 was an anomalous year, fueled by record recent exits, inexperienced early-stage investors and FOMO-fueled market tourists who contributed larger cashflows to startups directly and via investment in venture funds than any time in recent memory.

- Global political and economic crises deflated the 2021 funding bubble with increasing force over the course of 2022, reaching a low (so far) during the second half of the year. Overall, funding fell 35% annually, and nearly 60% comparing Q4’21 and Q4’22. In many markets, valuations declined by 50% or more, returning to pre-bubble (2016 – 2019) levels.

- Deal power is now shifting from founders to investors, returning to pre-bubble levels of more balanced investor/founder terms.

- 2022 was a correction, not a collapse. Valuations aside, 2022 was still a year in which venture and angel funding were comparatively high, compared to most years except 2021. At the same time, the correction is still happening: most indicators—a closed IPO window, increased fire sale M&A, SPAC failures, pay to play rounds, tech sector layoffs, plummeting public market valuations and falling funding levels in the US and globally—are still trending negative.

Key Takeaways:

- Burn the 2021 deal playbook. It was an anomalous year and should not be used by angels as the basis for valuation, market comparables or deal terms. In evaluating a company’s valuation ask, ensure that the data used are not weighted by 2021 comparables.

- Diligence and Governance Matter More than Ever. Capital raised and valuations are only two elements of an overall deal. If anything, the past few years highlight the need for strong corporate governance and real diligence. Don’t let FOMO persuade investors to abandon angel diligence best practices. And don’t execute deals that deliberately exclude angels from startup governance. Real corporate governance is needed to manage tough financings, predatory investors, company restructuring and inevitable M&A market consolidations.

- The Malaise is Winding Its Way Through the Private Capital Value Chain. The decline in deal volumes and valuations first hit unicorns, then pre-IPO and late-stage companies and is working through the venture ecosystem. First to rise, first to fall. At present, angel/seed stage has only recently begun to be affected and not as sharply as other stages (so far). It is unclear if late 2022 declines in angel and seed funding will stabilize or decline further.

- High Deal Valuations Depend on Expectations of High Returns. High valuations are only justified if investors believe that high exit multiples will remain the norm several years from now. But these multiples have already declined sharply. Valuations have returned to “normal” (2016-2019) ranges. Unless we enter another explosive bull market, it is doubtful that valuations will “recover” anytime soon to 2021 bubble levels. The exit markets fueling higher valuations are essentially closed. And valuation analysis has also become more sophisticated. The investor exit calculus increasingly includes expectations about exit sustainability. Why? Most 2020/21 IPO and SPAC exits did not hold their value in the months after the exit, leading to increased caution among investors who buy IPO shares.

- We Warned You! Experienced angels cautioned CEOs in 2020-2021 that sky-high valuations would cause fundraising pain if bubble markets deflated. As predicted, CEOs who closed rounds in 2020/2021 at outsized valuations are finding fundraising difficult.

- A Flood of Companies Will Try to Raise Capital in 2023. A recent startup survey cited by Bloomberg indicated that 80% of US and UK startups lack capital to last for a year. 2023 will be a very competitive year for startups seeking funding.

- CEOs Face Tough Choices: Take a down round now and suffer near-term pain or accept a structured financing deal with higher liquidation preferences and other terms which distort capital structures long-term. Or they can seek venture debt with its covenant-based downsides.

- Triage! For investors, it is triage time, focusing capital and support on those most likely to survive and thrive during this downturn. And triage will apply to deal flow, not just existing portfolio companies. It is a good bet that investors will fund fewer undifferentiated “me-too’s” versus startups solving critical problems using deeper tech and more hard science.

- Stronger Survivors. 2023 will likely be a year of company failures for some and restructuring for others. The survivors will place greater focus on core products, services, more efficient processes and strategies to gain market share even in tougher times. Those who do this well will emerge stronger and more competitive. In 2023, average valuations for the smaller number of companies who successfully raise funds are likely to rise as those who pass muster will likely be more solid companies who have demonstrated stronger performance and better metrics during a tougher diligence cycle.

- But it is Still a Great Time to Be an Angel. Even In today’s market, seed and early stage remain attractive for prudent, value-added investors. Angel stage has been the most resilient, the least subject to wild swings in valuation or invested capital. And a recent ACA survey of angel groups indicated that most are staying the course and continuing to invest both in their existing portfolio and in new deals. Despite near-term crises, investors who have experienced earlier down markets know that today’s environment offers great opportunities to invest long term and to increase the odds of success by adding the kind of follow-on cash and “mentor-capital” in which angel groups excel, particularly for companies with sustainable value who are solving real problems that matter.