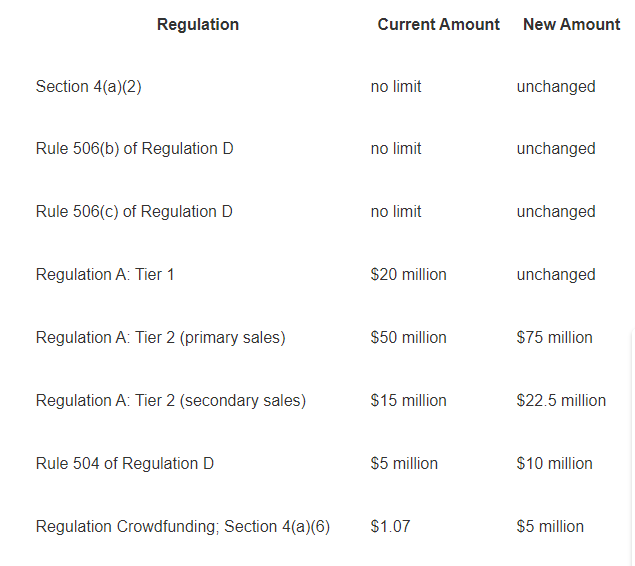

Tuesday, November 17, 2020 Tuesday, November 17, 2020 The Exempt Offering Ecosystem: What the SEC ChangedBy: Dror Futter, Legal and Business Adviser to Startups, Venture Capital Firms and Technology Companies The SEC announced a series of amendments (likely to be effective early next year) to the rules governing private offering exemptions – by far the most frequent path for venture fundraising. The amendments retain the same “menu” of exemptions but make incremental improvements. For the early stage community, the amendments include a very useful provision that excludes “Demo Days” from being considered general solicitations provided certain conditions are met. In the US, all securities offerings have to be registered with the Securities and Exchange Commission (SEC). This is a time consuming and expensive process that is unsuitable for most startup companies. To fill the funding gap, a series of exemptions exist that allow companies to fundraise without registration. The result is a complex menu of options, each with its own limitations and requirements. The conditions on funds raised through one of the exemptions typically include one of the following points: 1. Limits on What Can Be Raised Within a 12 Month Period 2. Post-Issuance Restrictions on Resale 3. Investor Requirements (is the exception available to unaccredited investors) 4. Does the Exemption Preempt State Registration Requirements? 5. Can Fundraising Under the Exemption Include “General Solicitation”? 6. Are Filings with the SEC Required? What often makes the framework challenging for companies seeking to fundraise is that each of the exemptions has its unique combination of conditions. On November 2, the SEC announced amendments that will implement a series of changes to the regulations to “harmonize, simplify, and improve the multilayer and overly complex exempt offering framework.” Although the exemptions remain complex, the changes provide incremental improvement to the existing framework. Almost all of the new rules should become effective early next year. At the end of this article is a chart, provided by the SEC in the press release announcing in amendments, that summarizes the keys terms of each exemption once the amendments are enacted.= The most significant changes: Increases in Annual Fundraising Amounts – to date, fundraising under Regulation A (Reg A+) and Regulation Crowdfunding (Reg CF) has had limited success. It will be interesting to see if the increase in fundraising limits results in increased usage.

Exclusion of Demo Days from Being Considered a “General Solicitation” – Demo Days in which startups fundraising “pitch” to potential investors have long been problematic due to restrictions on “general solicitations” applicable to several of the exemptions. Pursuant to the amendment, an issuer would not be deemed to have engaged in general solicitation if the communications are made in connection with a seminar or meeting sponsored by a college, university, or other institution of higher education, a local government, a nonprofit organization, or an angel investor group, incubator, or accelerator. Under the new rules, the term “angel investor group” means a group: (A) of accredited investors; (B) that holds regular meetings and has written processes and procedures for making investment decisions, either individually or among the membership of the group as a whole; and (C) is neither associated nor affiliated with brokers, dealers, or investment advisers. The Demo Day sponsor is not permitted to: • Make investment recommendations or provide investment advice to attendees of the event; • Engage in any investment negotiations between the issuer and investors attending the event; • Charge attendees of the event any fees, other than reasonable administrative fees; • Receive any compensation for making introductions between attendees and issuers, or for investment negotiations between the parties; • Receive any compensation with respect to the event that would require it to register as a broker or dealer under the Exchange Act or as an investment adviser under the Advisers Act. In addition, the advertising for the event may not reference any specific offering of securities by the issuer, and the information conveyed at the event regarding the offering of securities has to be limited to: • Notification that the issuer is in the process of offering or planning to offer securities; • The type and amount of securities being offered; and • The intended use of the proceeds of the offering. Other Modifications

This article originally appears in Crowdfunder Insider. Dror Futter is a partner in the Rimon, PC law firm. Dror’s practice focuses on representing startup companies in their financing and merger and acquisition transactions and their intellectual property, IT and internet agreements. He also advises companies with respect to Initial Coin Offerings and other blockchain legal issues. Dror was the co-founding chair of the PLI VC Law program and hosted their first blockchain legal program. He is a frequent speaker and writer on blockchain legal topics. He is a member of the model forms drafting group of the National Venture Capital Association, the legal advisory board of the Angel Capital Association and the legal working groups of the Wall Street Blockchain Alliance and the Digital Chamber of Commerce. Dror can be reached at dror.futter@rimonlaw.com |