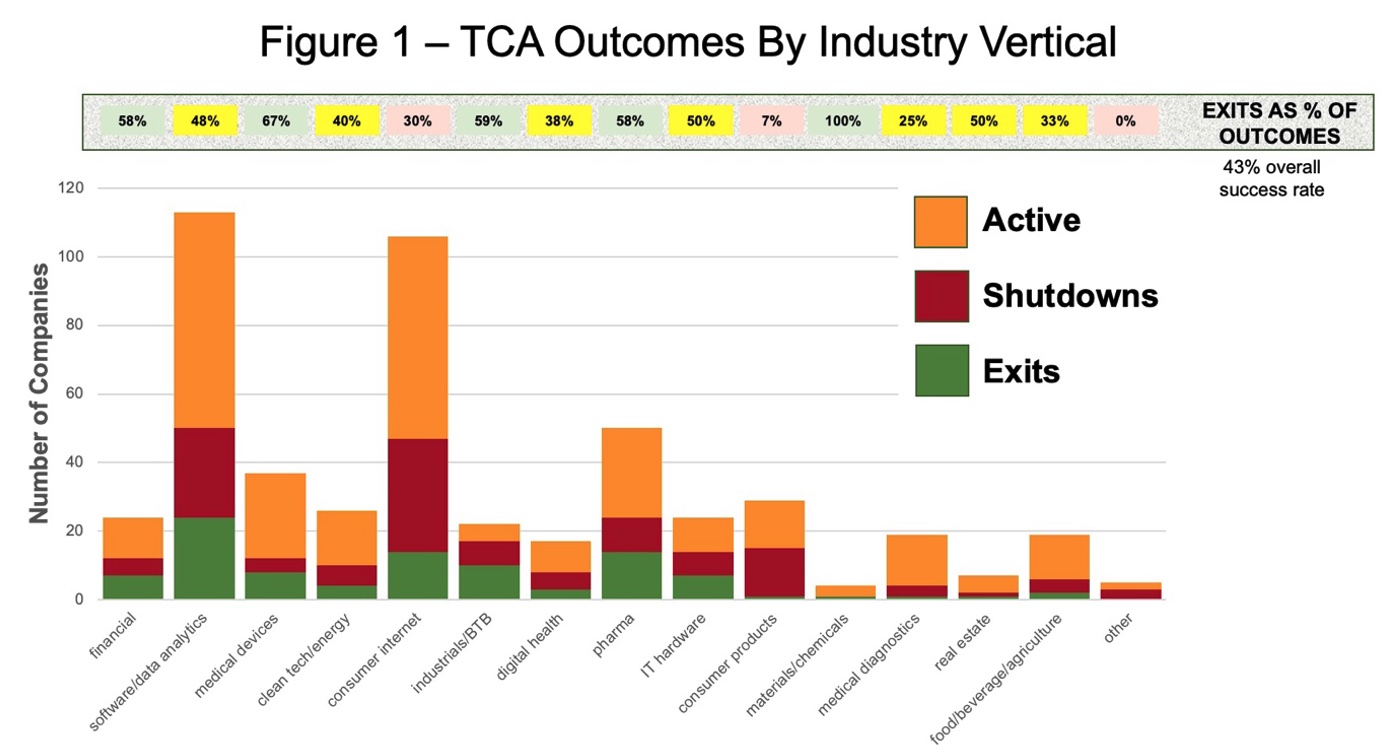

Wednesday, February 07, 2024 Wednesday, February 07, 2024 Do Some Industry Verticals Produce Better Returns Than Others?As angels, we see opportunities in many different industry verticals. We ask ourselves why some verticals produce better returns than others? This article looks at the experience that TCA Venture Group (formerly Tech Coast Angels) has had on all their 247 outcomes from 1997 – 2022 for insights. First of all – an important caveat. While 247 seems like a statistically significant number, when that is sliced into 15 industry verticals it becomes less statistically significant in each vertical – particularly when returns in this asset class are driven by a few homeruns. Nevertheless, this author believes that some interesting insights can be gleaned and are hence worth sharing. Back to the analysis. Of the 526 companies in TCA’s portfolio at the end of 2022, 279 were active and the remaining 247 outcomes included 141 shutdowns and 106 exits. Exits are defined as having at least some cash returned (but does not include acquisitions for stock). Figure 1 shows how this breaks out by industry vertical, including the percent of outcomes that are exits: Figure 1: TCA Outcomes by Industry Vertical

Source: Analysis of all 526 TCA Venture Group portfolio companies 1997-2022 Software/Data Analytics and Consumer Internet verticals each have over 100 portfolio companies, but the 48% percent exits as a percent of outcomes for Software is dramatically higher than for Consumer Internet (30%). The Financial Services vertical has far fewer investments (24) but an even higher (58%) exits as a percent of outcomes. Pharma (58%) and Medical Devices (67%) are other verticals with a high exits as a percent of outcomes. Consumer Products (7%) has the lowest exits as a percent of outcomes of all the verticals. Why these differences? Here are some hypotheses:

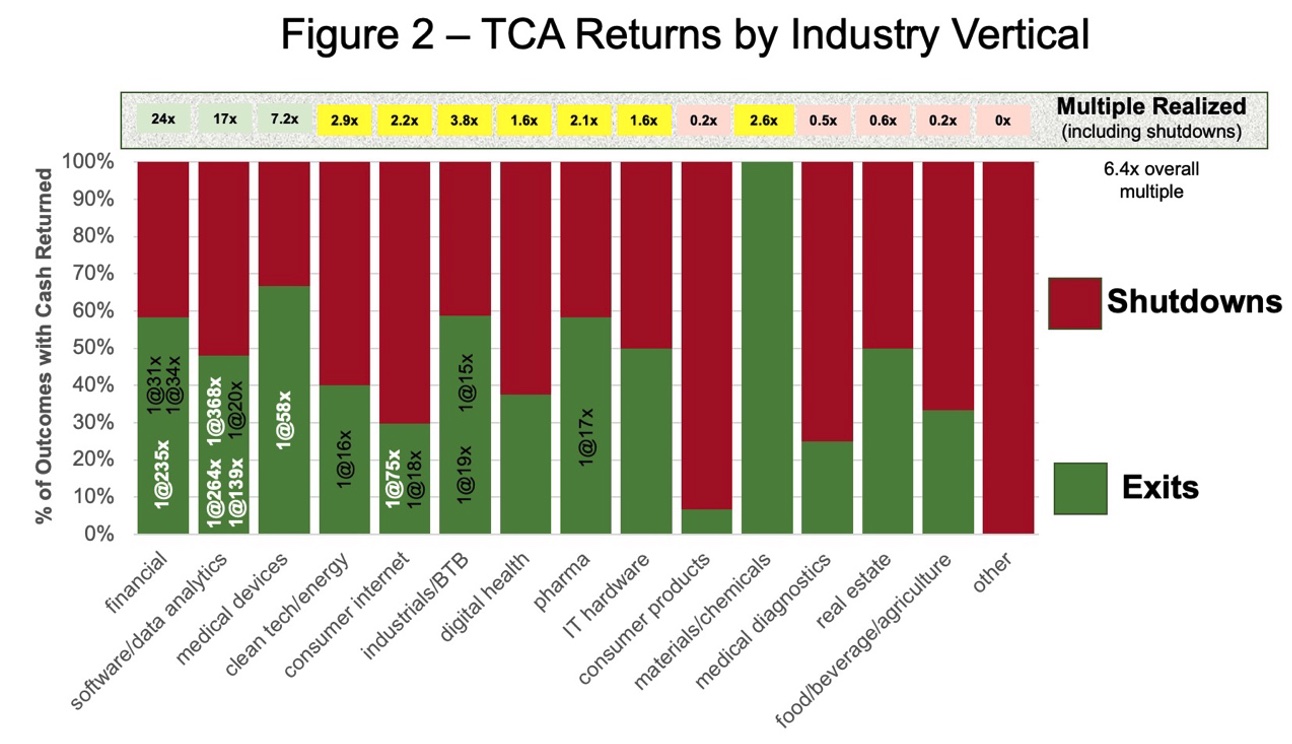

The other observation from Figure 1 concerns what percentage of investments realize an outcome of any sort. Notably, both Software and Consumer Internet have a high percentage of active companies, and this is perhaps due to these companies being able to become self-sufficient yet not enough traction to realize an exit. Medical Device, Pharma and Medical Diagnostics also have a high percentage of active companies, and this is perhaps due to the long time required to win FDA approval (thus they stay active in the portfolio longer). Food/Beverage/Agriculture also has a high percentage of active companies, perhaps because it takes longer to be noticed; however, big returns can be possible, such as Apeel Sciences which is one of the unicorns ($2.5 billion valuation) in TCA’s active portfolio and has been around more than a decade. Turning to returns, Figure 2 shows returns by industry vertical: Figure 2: TCA Returns by Industry Vertical

Source: Analysis of all 247 TCA Venture Group portfolio companies with Outcomes (Exits or Shutdowns) 1997-2022. The two verticals that have produced the best returns for TCA investors have been Financial (24x) and Software (17x). Our four largest multiples realized have been in those verticals, with 368x for Procore Technologies, 264x for Mindbody, 235x for GreenDot and 139x for Sandpiper. The only other vertical with an average return above TCA’s 6.4x average is 7.2x for Medical Devices which was buoyed by Companion Medical at 58x. All of the verticals that realized returns of 3.8x or greater had at least one “home run”(defined here as 50x or better), and all the verticals that realized less than 2x on average had no “home runs.” So it is certainly possible that a vertical such as consumer products might have a “grand slam home run” but they tend to be very rare in that vertical – one of the few that I can think of was the sale of Nest thermostats to Google for $3.2 billion. But it is safe to say that exits in Consumer Products above $20-30 million are exceedingly rare compared to the frequency of larger exits in Software for example. This might be because Consumer Products can be capital intensive (working capital investments in inventory and accounts receivable) compared to software, where margins are extremely high, revenues can grow faster, there are no working capital requirements, no cost of goods sold, the valuation multiple on revenues is hence much higher; and a software business can scale quickly without a lot of additional capital (unless it is a business such as AI that has huge computer processing costs). Again, this does not mean that you can’t have a home run in Consumer Products, but the odds of that happening are lower than in Software. For this reason, it is not surprising that VCs invest much more dollars into Software companies compared to their investments in Consumer Products companies. Food/Beverage/Agriculture has the lowest realized multiple of 0.2x, partly for similar reasons as Consumer Products because this vertical includes a lot of food products that are sold in grocery stores and hence have many of the same limitations. Looking to the future, this might change for TCA if and when our one unicorn in that vertical (Apeel Sciences) gets to a liquidity event. We had one rare home run (75x) in consumer internet with Truecar (formerly ZAG.com), but other than that, the returns have been sub-par in that vertical. Understanding the reasons for the differences helps inform us as to what questions are worth probing in each vertical. For instance, for a Consumer Products company, what is their plan to raise sufficient working capital for inventory and accounts receivable if they are successful at penetrating a major retailer? Personally, I’ve invested in two Consumer Products companies that failed after growing to several million dollars in revenue before getting an order for 400 + pallets of product when they had success in earning their first Costco order but then lacked the needed capital and soon after went out of business. When doing due diligence in this vertical I look beyond the initial placement in a channel such as Whole Foods and try to understand the customer repeat rate and re-order rate by the retailer. Every successful company I can think of with revenues has achieved high retention rates of customers, and that is often the difference between the exits and shutdowns because cost of acquiring new customers tends to be high. It's hard to fill a bucket with a bunch of leaks in it. Takeaways

AUTHOR: John Harbison , Chairman Emeritus of TCA Venture Group (formerly Tech Coast Angels), ACA Board Member. Tags: |